{kind=link}

Automation in Insurance Claims: Speed, Accuracy, and the New Normal

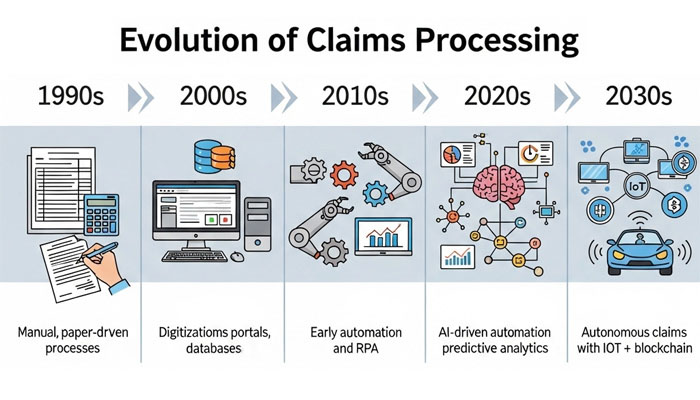

The insurance claims process has always been at the heart of customer trust in the financial services industry. For decades, it was defined by paperwork, lengthy investigations, and delayed payouts — often leaving policyholders frustrated and insurers struggling with efficiency. Today, however, the industry is entering a new era where artificial intelligence (AI) and automation are no longer futuristic add-ons but central pillars of operational excellence.

The conversation around AI in insurance claims has shifted dramatically in the past five years. From experimental pilots to enterprise-wide adoption, insurers now view AI and automation not just as cost-saving tools but as strategic enablers of customer satisfaction, fraud detection, and sustainable growth. The transformative potential lies in how these technologies are reimagining claims — turning them from a pain point into a differentiator.

AI in Claims: From Hype to Real Impact

For years, AI in insurance claims was discussed in theory — predictive algorithms, image recognition, and robotic process automation (RPA) that could streamline adjuster workloads. But the question lingered: could technology truly replicate the complex, human-driven decisions in claims assessment?

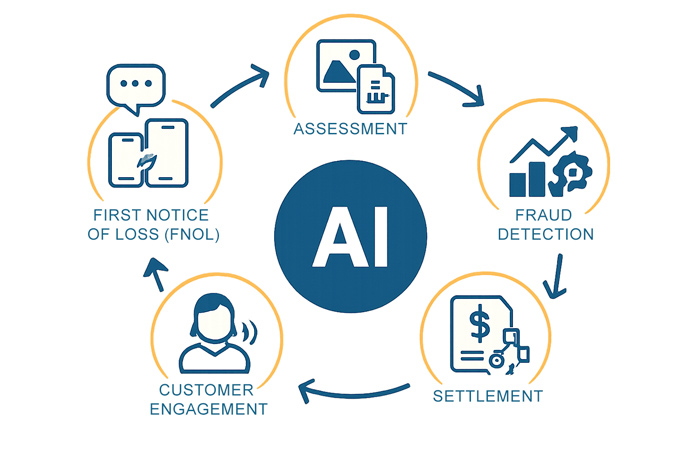

The answer is increasingly clear. AI is now deployed across the claims lifecycle, from first notice of loss (FNOL) to settlement. In auto insurance, image recognition powered by computer vision can analyze accident photos and estimate repair costs within minutes. In health insurance, natural language processing (NLP) extracts relevant data from medical records, ensuring claims are adjudicated faster and more accurately.

The result is more than just efficiency gains. By reducing manual effort, insurers can dedicate human expertise to complex cases while allowing automation to handle routine ones. This shift is not about replacing adjusters but about elevating their role.

The Rise of Intelligent Automation

While AI drives intelligence, automation ensures speed and consistency. Robotic process automation has become the backbone of modern claims management, performing repetitive tasks like data entry, policy verification, and document classification. When combined with AI, automation evolves from simple rule-based processing into something far more powerful — intelligent automation.

For example, an automated claims intake system can instantly gather policyholder data, validate coverage, flag potential inconsistencies, and even predict settlement timelines. Instead of spending weeks gathering information, insurers can now process simple claims in hours or even minutes.

This isn’t just operational optimization. Intelligent automation fundamentally redefines the customer journey. A policyholder filing a claim after a car accident can upload photos, receive an AI-generated damage assessment, and get payout approval the same day. What was once a stressful and drawn-out ordeal is now seamless, transparent, and customer-centric.

Case Studies: Global Adoption of AI in Insurance Claims

Several leading insurers are already setting the benchmark for how AI and automation reshape claims.

- Ping An (China): One of the pioneers, Ping An uses AI-driven image recognition for auto claims, with some settlements completed in under three minutes.

- Allstate (USA): Through machine learning models, Allstate predicts claim complexity, enabling smarter resource allocation. Simple claims are automated, while human adjusters focus on nuanced cases.

- Allianz (Europe): Allianz integrates AI with customer-facing apps, allowing policyholders to interact with virtual assistants that guide them through claim submissions in real time.

These examples demonstrate that AI in insurance claims is not confined to experimental labs. It is being deployed at scale, shaping customer expectations worldwide.

Balancing Efficiency and Empathy

Yet, for all the advances, one central challenge remains: maintaining the human touch. Insurance is not just a transaction — it’s often triggered by moments of crisis, such as illness, accidents, or loss. No algorithm can fully replicate empathy or the reassurance of a human voice.

This is why successful claims strategies blend AI and automation with human oversight. Automation handles the “heavy lifting” of data processing and routine communication, while claims professionals step in to provide guidance, compassion, and judgment when it matters most. The result is not a replacement of human roles but a redefinition of them.

The Role of AI in Fraud Detection

Fraudulent claims continue to be a multi-billion-dollar challenge for insurers worldwide. AI brings a new level of sophistication to fraud detection by analyzing patterns across massive datasets.

Machine learning models can identify anomalies in claim submissions, cross-reference historical records, and flag suspicious activities in real time. Predictive analytics further help insurers proactively address fraud before it results in significant losses.

This not only saves costs but also protects honest policyholders, ensuring that resources are directed where they are needed most. AI in insurance claims is, therefore, as much about trust and fairness as it is about efficiency.

Regulatory Considerations and Ethical Questions

As with all transformative technologies, AI and automation raise important regulatory and ethical considerations. Issues such as algorithmic bias, transparency in decision-making, and data privacy remain under scrutiny. Regulators are increasingly pushing for explainability in AI models, requiring insurers to ensure that automated claim decisions are fair, traceable, and accountable.

The balance between innovation and compliance will define the next phase of adoption. Insurers that embrace responsible AI — prioritizing fairness, transparency, and data security — will gain both regulatory approval and customer trust.

Future Outlook: Toward Autonomous Claims

Looking ahead, the trajectory points toward autonomous claims — a future where entire claim journeys, from FNOL to settlement, can occur with minimal human intervention. With the integration of Internet of Things (IoT) devices, connected vehicles, and blockchain, the ecosystem of claims is becoming interconnected and real-time.

Imagine a connected car that detects an accident, instantly notifies the insurer, shares telematics data, and initiates an AI-driven claim. Repair shops receive work orders, payments are processed digitally, and the policyholder is kept informed throughout — all without filling out a single form.

While this vision is still unfolding, the foundations are already here. Insurers investing in AI and automation today are building the capabilities that will define the industry’s future.

Conclusion

The insurance industry is at an inflection point. The convergence of AI and automation is not just making claims faster; it is redefining the very nature of the process. Efficiency, accuracy, fraud prevention, and customer experience are no longer competing priorities but interconnected outcomes of intelligent claims management.

For insurers, the message is clear: embracing AI in insurance claims is not optional. It is a strategic imperative. Those who move decisively will not only improve operations but also earn the trust and loyalty of customers in an increasingly competitive landscape.