{kind=link}

Getting a payment to a supplier is often still more complex than it needs to be for something so basic to running a business.

In many organisations, invoices get passed from inbox to other inbox, approvals get lost in email processes, and finance teams use up their valuable time matching payments against records. What should be a routine cycle becomes disorganised, limiting visibility, binding working capital and adding around 8-15% in collection costs for organizations that depend on manual processes.

The impact is much wider compared to the finance function. Buyers are considering internal controls against the requirement to manage liquidity. Often suppliers are waiting 30 to 45 days or more to get paid, putting a strain on cash flow and restricting their ability to make investments, hire or grow. For many businesses those delays are functional, rather than being occasional.

Bridging the acceptance gap when it comes to commercial payments

It is indeed clear that commercial cards are a boon for business. They can help streamline processes, enhance control and offer greater flexibility in working capital. In the past, however, the acceptance of B2B suppliers has limited the scope of those benefits.

Some businesses are content to take cards, but many smaller and cross-border organizations still run via conventional account-based payment methods. This means companies frequently have to deal with a patchwork of digital as well as manual payment processes throughout their supplier base.

The practical problem calls for solutions that fit within current commercial processes, not asking all participants in the environment to alter how they operate.

Digitization across the supply base

This is where modern forms of payments are helping fill the gap.

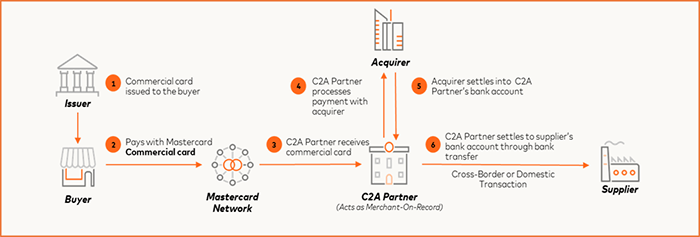

For instance, Card to Account – C2A frameworks decouple the initiation of a payment from the receipt of a payment. With a commercial card, a buyer can pay in any marketplace or currency, and the supplier gets paid straight into their bank account without having to authorise cards or change how they invoice customers.

The benefits cascade through the ecosystem –

- Enhanced flexibility for buyers when it comes to working capital and cash flow management.

- Payment and approval flow can be incorporated into existing systems so minimal manual efforts are required.

- Reconciliation gets better as transactions are recorded digitally from end to end.

- Suppliers continue to receive money via the channels they know, without altering their current processes.

Ecosystems based on networks, like the Mastercard Card to Account Partner Program, are making it possible to do that at scale. These programs connect buyers and banks as well as speciality service providers to get commercial payments into supplier networks that historically have been challenging to digitize without hassle or risk.

From limitation to flexibility

The change is most evident in the way firms take care of liquidity.

For example, one large Asia Pacific telecommunications company experienced working capital limitations during peak demand times. Supporting growth also meant increasing payables, but not at the cost of supplier relationships or operational intricacy.

It has launched a card-to-account solution with fintech partner ipaymy in a matter of weeks, with no system integrations. No change to invoicing or payment reconciliation. Suppliers were paid directly into their current accounts.

According to the CEO of ipaymy, Olivia Leong, ” We went from the first conversation to live transaction in under 60 days unlocking over 50 days of interest-free working capital for the business, with zero disruption to suppliers. Speed of implementation and immediate access to liquidity: that is what the card-to-account program delivers.”

The outcome was a more agile liquidity structure that allowed the telco to absorb spikes in demand and release capital in bulk without putting any sort of pressure on the supply chain.

Embedding confidence into more intricate payment flows

As these frameworks grow, so does the intricacy of payment flows. Transactions can involve many parties, right from buyers and suppliers to platforms and financial institutions, across borders. It calls for visibility at all times, strict compliance controls and unambiguous accountability of how funds move.

Governance happens to be a design core, not a back-end necessity, driven by increasing demands around anti-money laundering safeguards, know-your-business guidelines and integrity of transactions. Structured partner ecosystems with standardized onboarding and ongoing monitoring are important to guarantee that payments are executed as intended.

Designing what lies ahead

Businesses are required to have payment systems that work throughout the markets, plug into current processes, and accommodate diverse supplier networks without adding any complexity.

In order to meet these expectations, one will require deeper collaboration like integration of global payments rails, fintech capabilities, and institutional frameworks at scale. One path forward is via approaches like the Mastercard Card to Account Partner Program, which does not replace current systems but rather links them more efficiently and extends their footprint.

It is not just the mechanics of payments that are changing, but also what they allow for organisations. Commercial payments can work across the entire spectrum of business interactions, far beyond the confines of current acceptance norms.

The Mastercard Card to Account Partner Program is at present available in selected Asia Pacific markets.